A pattern many leaders recognise: income is steady or rising, the team is busy, service activity looks healthy. And yet cash feels tighter than it should. Small cost increases create disproportionate stress. The financial confidence the numbers suggest never quite arrives.

This is rarely a fundraising or sales problem. It’s a structural one — and once you can see it, it’s usually fixable.

Revenue and margin are different disciplines

Revenue measures volume. Margin measures efficiency, pricing and cost control. Most organisations track the first carefully and the second only loosely — which is why income can climb while the margin underneath it gets thinner.

For charities and social enterprises this shows up in familiar ways: more contracts won, but each one squeezed on price. Larger grant portfolios with more conditions and less core-cost coverage. New trading activity that looks healthy at the top line but consumes a disproportionate share of senior leadership time.

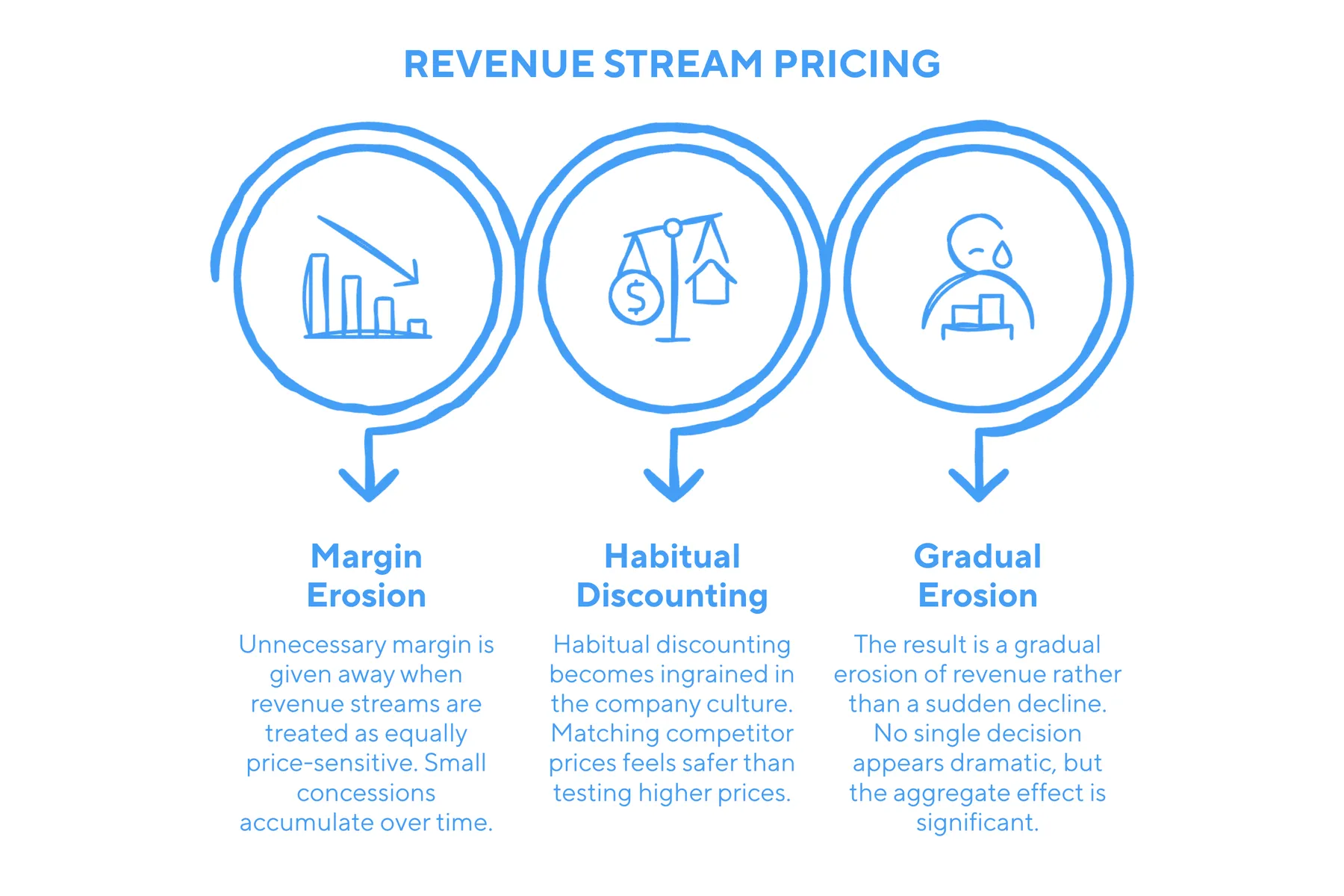

Where the leak usually starts

Three patterns turn up again and again.

Pricing by habit, not by evidence

Discounting becomes cultural — preserving a relationship, matching another provider, closing the deal quickly. None of these decisions look dramatic in isolation. They accumulate.

Treating all income streams as equally price-sensitive

Some services can sustain higher prices with little impact on demand. Others can’t. When you treat them as the same, you give margin away unnecessarily.

Complexity creep

As organisations grow, services expand, customised offerings multiply and legacy programmes stay in place. Each addition looks rational in isolation. Few leaders step back to look at contribution margin across the whole portfolio. Revenue rises; profit stagnates because resources are spread too thinly.

The result is gradual rather than dramatic. No single decision compresses margin sharply. The aggregate effect is significant.

From reaction to diagnosis

Most leaders, faced with a margin problem, reach for one of two levers: across-the-board cost cutting or general price increases. Both are blunt.

A more rigorous approach starts with diagnosis. Pick one service or income stream and analyse it properly. What does true contribution margin look like once you’ve included senior leadership time and operational overhead? Were recent pricing decisions strategic, or reactive? Were price changes tested against actual demand sensitivity, or assumed?

You usually find one of two things: an offering that could sustain a higher price without losing volume, or one whose underlying economics no longer work — a candidate for repositioning, restructuring or letting go.

Pricing is not just a number

Customers, funders and commissioners read price changes through a lens of fairness as much as cost. The reason given matters as much as the figure. Leaders who explain clearly how pricing supports service quality, access or operational stability tend to find that acceptance follows.

The real question isn’t whether to raise prices or cut costs. It’s whether pricing decisions are grounded in evidence and aligned with where the organisation is trying to go.

Two questions before the next planning cycle

- Where have pricing decisions been driven by assumption rather than measured demand sensitivity?

- Are revenue targets being optimised at the expense of contribution margin?

Revenue creates visibility. Margin creates resilience. In uncertain markets, resilience determines which organisations keep control of their direction and which spend the year reacting to pressure.

Pick one service area. Run the diagnosis. The leak is usually small enough to fix once you can see it.